Today we are talking about your chargeback rights. It’s impossible to deny the fact that chargebacks are one of the most inconvenient merchant’s issues. Undoubtedly, banks are on the customers’ side when it comes to a dispute. Moreover, the whole concept of the “chargeback” was created to protect the customer in the first place.

However, it doesn’t mean that you as a merchant need to give up! Did you know that a trite misunderstanding results in 49% of chargebacks based on friendly fraud? Simply put, the customer had no clue s/he was filling in the chargeback form. Or that 81% of customers fill in the form because it’s easy? That means customers don’t want to use other options like, for instance, contacting the merchant directly to solve their issues.

Fair to say, these reasons must not result in your revenue loss. That’s why knowing your chargeback rights is vital. In this article, we will talk about:

- chargeback process parties,

- your main rights, as a merchant,

- what may violate your rights,

- and how to fight chargebacks.

Of course, using chargebacks prevention tools is the best option to protect your business. Nevertheless, knowing your chargeback rights is a powerful asset as well. So, let’s dive in!

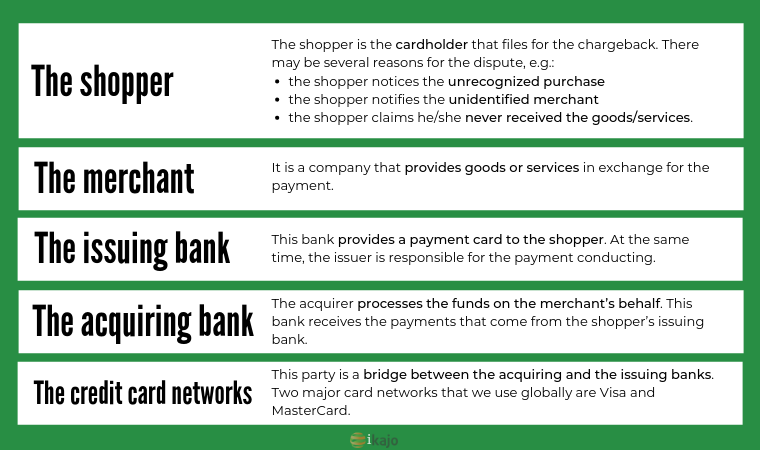

What are the chargeback process parties?

Chargeback serves as a cardholders’ protection from fraudulent activity committed by other individuals or merchants. These are the parties that take part in the chargeback dispute process.

What are merchants’ chargeback rights?

Since different merchants sell different goods and services, the reasons for filing a chargeback may vary. However, there are the so-called chargeback reason codes (Visa Claims Resolution and MasterCard Chargeback Guide), which are commonly used as the main dispute base.

In the chapter below, we’ll group some primary chargeback causes. We dare to hope that you work ethically, in which case, you can fight these chargebacks. For now, let’s take a closer look at your rights.

- You have 15 days to facilitate the reimbursement. It’s applicable if the shopper doesn’t like a product and returns it within the determined period. The issuer cannot file a chargeback earlier. As a result, the merchant has enough time to eliminate a dispute.

- You must not reimburse more than the original price. Regardless of the refund the shopper wants to receive, the issuer cannot surpass the amount of the initial transaction. There are only some options the issuer can file for:

- the full original transaction amount,

- the full transaction amount divided into several chargebacks repayments,

- the partial amount of the original transaction.

N.B. In some cases, the merchant must repay handling or shipping fees, alongside accompanying fees paid by the shopper.

- You must not fulfill the chargeback request if the customer doesn’t meet T&C. It implies that the shopper must file for chargeback within a fixed period.

- You are not responsible for the cashback transactions. The shoppers cannot file the dispute for any kind of cashback transactions.

Also, there are two cases when the shopper has to contact the merchant first.

- If the purchase arrives after the stated delivery period. First, the shopper should try to return the product. The issuer has to make sure there was such an attempt before processing the chargeback.

- If the selected number of the chargeback reason codes. Many codes require to contact the merchant and solve the problem with him first. Should both sides not find a solution, the shopper can file for the chargeback.

Knowing of these rights is the key pillar of your success in case of a dispute. Nevertheless, make sure to provide a prompt response to your customers if they face any problems. Quality customer support is your protection against chargebacks.

What violates the merchant chargeback rights?

So, you’ve learned your rights and are ready to fight back. Unfortunately, there are some cases when you cannot beat the system.

- Chargeback fraud (friendly fraud). Think of these numbers – 1) friendly fraud causes 86% of chargebacks, 2) friendly fraud increases by 41% every two years. All-in-all, the mechanism, created to protect the shoppers, results in complications for merchants.

Surprisingly, customers do not intend to cause your company any troubles. Usually, they simply mix up a ‘refund’ with a ‘chargeback’. Or fill in the chargeback form because it seems easier than contacting the merchant directly.

- Lack of proper chargeback reason codes. Though the credit card networks have a vast choice of codes, loopholes still happen. In this case, the customer files for the pre-compliance chargeback (aka reason code 98). This code collects all the exceptions under its wing.

The great piece of news for the merchant is that the pre-compliance dispute doesn’t influence the chargeback ratio.

Representment

Last but not least is representment which stands for the merchant’s right to fight chargebacks. Remember, this is a substantial option that eliminates extra spendings. To make it clear, merchants lose $2.40 for each dollar involved in the chargeback reimbursement. And we don’t want to let this happen to you.

What are the stages of the representment process?

- The merchant re-presents the dispute to its acquiring bank. It must include the documentation that supports the chargeback case.

- The acquiring bank passes the representment to the issuing bank after the evaluation. The issuing bank estimates the case once again.

- In case of complete evidence and corresponding chargeback reason code, the issuing bank is likely to satisfy your representment.

N.B. The understanding of the chargeback reason codes is a powerful tool for merchants. It helps to fight chargebacks in the most efficient way possible.

Conclusions

All things considered, knowing of chargeback rights is highly important for merchants. This knowledge empowers them when it comes to dispute management. Ikajo recommends you to do your homework and learn chargeback reason codes (get more about them from Ikajo’s fresh article). Moreover, opt for the payment processor with trusted chargeback prevention tools.

Now it’s time to hear from you. Have you ever faced chargeback claims? What are your go-for methods of solving them?

Leave a comment and let’s discuss your rights. Because the main aim of Ikajo, as a payment processor, to protect you from the chargebacks. By all available means.